Asset Location Strategy: The Missing Piece of Tax-Efficient Investing

- Ryan A. Dunn, CFP®

- 13 hours ago

- 5 min read

Key Takeaways

Asset location determines which types of accounts (taxable, tax-deferred, tax-exempt) are best for holding those investments to maximize your after-tax returns.

Most investors overlook asset location, yet it can save thousands in taxes annually and significantly boost long-term wealth.

Placing the wrong assets in the wrong accounts creates unnecessary tax burdens that compound negatively over decades.

Asset location – not to be confused with asset allocation – is something we bring up with all our new clients. It’s a powerful tool that helps clients save lots of money in taxes over the life of their plan and substantially boosts their returns.

As most of you know, asset allocation determines your optimal mix of investments (stocks, bonds, cash, real estate, and other assets) to manage your risk and return. Asset location is something entirely different. Asset location determines which types of accounts (taxable, tax-deferred, tax-exempt) are best for holding those investments to maximize your after-tax returns. At Novi, we believe both asset allocation and asset location are essential for portfolio management, with location acting as a tax-efficient strategy.

I like to think of the difference as follows: Asset Allocation = what you own and Asset Location = where you own it.

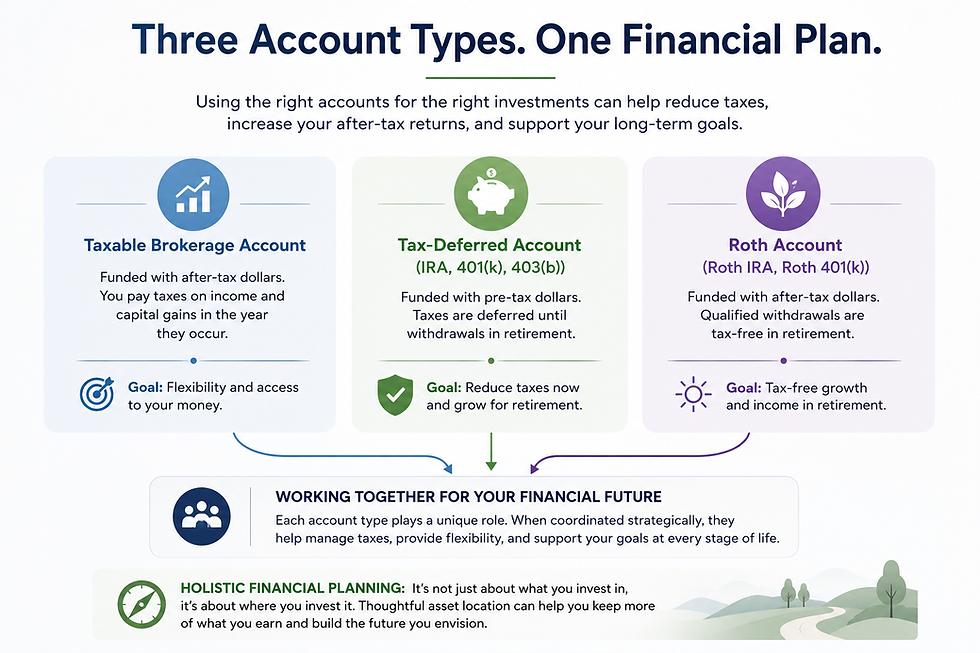

Most people have their investments in one of three types of tax buckets:

1. Taxable Brokerage Account. Here you pay taxes annually on the interest and dividends you earn at your ordinary income rate. When you sell your holdings, you're paying taxes on the growth of your holdings at your capital gains rate.

2. Tax-Deferred Account. This includes your IRAs, 401(k)s, and 403(b)s. Your contributions (typically from your paycheck) reduce your taxable income in the year you make the contribution, and then you don’t have to pay tax on the money until you start taking withdrawals, typically in retirement, as well as your required minimum distributions. Unfortunately, in a tax-deferred account, those withdrawals and distributions are taxed at your ordinary income rate.

3. Roth Accounts are funded with after-tax money, so you don’t have to pay taxes on the principal, dividend, interest or growth when you go to take that money out. Sounds great, but if you earn too much money, you may not qualify and there are often low limits on how much you can contribute.

How Asset Location Works

An asset location strategy seeks to manage your total tax burden by pairing your tax-inefficient investments with your tax-advantaged accounts and by pairing your tax-efficient investments with your taxable accounts.

Tax-inefficient assets generate regular taxable events and thus cut into your return and silently eat away at your wealth.

For example, a retired couple with a $2 million portfolio ($1 million in a taxable account and $1 million in a tax-advantaged account) could potentially see a reduction in tax drag that equates to an additional $2,800 to $8,200 per year depending on their tax bracket.

Examples of tax-inefficient assets:

Real estate investment trusts (REITs), which must distribute at least 90% of their income to shareholders.

Core bonds, which issue regular income payments.

High-yield bonds, which also generate regular, potentially higher income.

However, by using a tax-deferred or tax-exempt account (such as an IRA, 401(k), or Roth) to invest in the assets listed above, you can shelter their distributions from annual taxes. This allows you to keep the money invested and to continue generating potential returns until you're ready to start withdrawing in retirement or when other life circumstances occur.

Once clients understand the concept of asset location preferences, they often ask me if they can park ALL of their assets in tax-advantaged accounts. I get it. But it’s usually not feasible because most tax-advantaged assets have annual contribution limits (such as an IRA or 401k), and some also have income restrictions. This means that wealthier investors must turn to taxable options such as brokerage accounts if they want to sock away more money for retirement.

Also keep in mind that there are downsides to tax-deferred accounts. When you take that money out, each dollar is taxed as ordinary income. So, we try to get high-growth assets into other types of accounts if possible. If those high-growth assets are placed in a tax-deferred account, it could lead to a large tax burden later in life.

However, even some “taxable” assets are relatively tax-efficient if they’re held in a taxable account. For instance:

Stocks that generate qualified dividends, which are taxed at more favorable rates.

Municipal bonds, which may generate tax-free interest.

Index funds, exchange-traded funds (ETFs) and tax-managed mutual funds that try to limit capital gains.

Investments you hold for over one year, which are subject to the lower long-term capital gains tax rates.

Research from Vanguard and the FPA Journal shows that utilizing asset location can improve your portfolio performance by 0.10% to 0.30% annually depending on the risk composition of the portfolio. That may not sound like a lot, but it adds up when compounded year after year. For instance, on a $2 million portfolio, even a modest 0.25% improvement could mean an extra $639,217 over 30 years. This assumes a 5% after-tax return vs a portfolio with a 5.25% after-tax return.

Asset location is most effective if you…

Have Significant Taxable Investments: If you have a substantial portion of your investments in taxable accounts.

Have a Long Time Horizon: The benefits of asset location compound over time, making it more impactful for long-term investors.

Are in a High Tax Bracket: The higher your tax bracket, the more you can benefit from tax-efficient strategies like asset location.

Invest in Varied Asset Classes: If you invest in a mix of asset classes with different tax treatments (e.g., stocks, bonds, REITs) asset location can be advantageous.

I know that asset location can sound confusing, so just keep in mind the big picture. This strategy allows you to put tax-inefficient vehicles or funds into tax-advantaged accounts. We’re using those taxable accounts or after-tax accounts primarily for equity exposure and maybe short-term bonds. We want to get as much growth as possible in the tax-free Roth accounts. Ideally, we’d like to execute the strategy immediately, but there are sometimes limitations due to underlying cost basis or underlying growth. But asset location is an ongoing process for Novi clients, and we continually work with them on it.

It can be very challenging to manage asset location by yourself using a spreadsheet. At Novi, we use powerful software that enables us to make proper decisions in situations when asset location makes sense. As we always tell clients: “focus on controlling the things we can control.” Asset location allows us to control portfolio construction while providing a reasonable “return” over long periods of time.

Conclusion

If you or someone close to you has concerns about your tax exposure or retirement readiness, don’t hesitate to reach out. I’m happy to help.

RYAN A. DUNN, CFP®, is a Wealth Manager at Novi Wealth