Is Doing Nothing a Strategy in Volatile Markets?

- Brenden Leese, CFP®

- May 14

- 4 min read

Key Takeaways

Market volatility triggers behavioral biases like loss aversion, recency bias, and action bias that often harm long-term financial success.

Take action for life changes, portfolio drift, or strategic opportunities like rebalancing, not for short-term, headline-driven market swings.

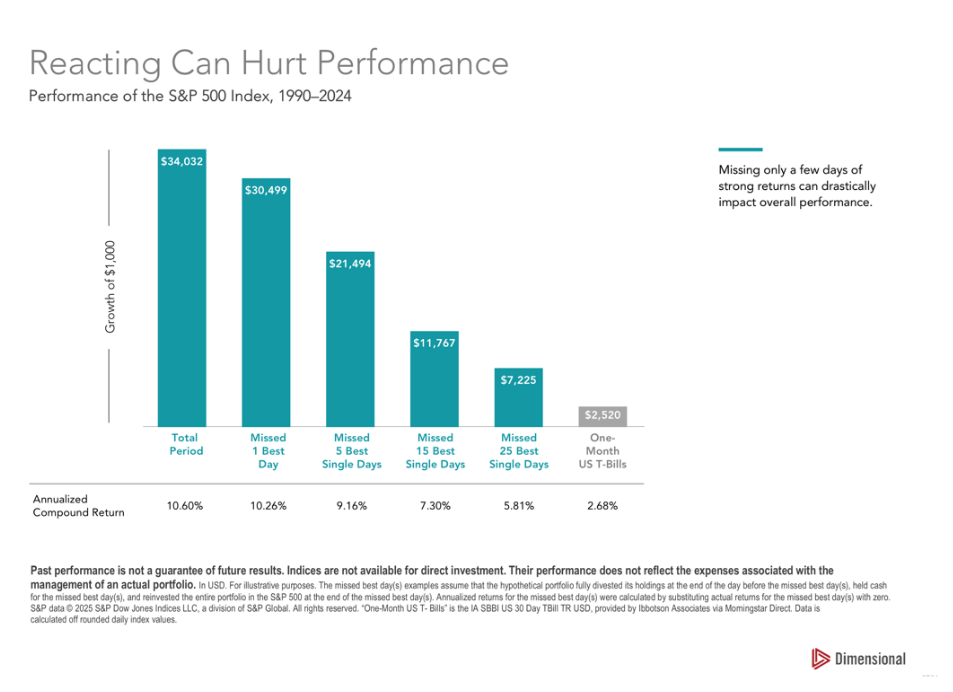

Missing the market's best days by going to cash can devastate growth of wealth; staying invested and diversified historically outperforms timing.

Since earning my behavioral finance designation as an Accredited Behavioral Finance Professional (ABFP), I’ve been fascinated by human behavior during times of stress. One of the biggest triggers of stress for people who are retired, nearing retirement, or in their peak earning years, is market volatility. And there’s been no shortage of that lately.

When people are fearful and sensing danger, it’s in our DNA to spring into action. Our fight or flight response kicks in and we want to flee from danger or do something ASAP to protect ourselves.

When markets are volatile, a number of classic behavioral biases kick in such as loss aversion, recency bias and action bias. These emotionally driven biases often lead investors to make emotionally driven decisions. These decisions often hurt the long-term success of their financial plans more than the market movements themselves.

Loss aversion states that investors feel the pain of a loss twice as strongly as the pleasure of a gain. This fear causes investors to hold losing positions too long, avoid necessary risks, and make irrational, emotionally driven decisions.

Recency bias causes people to overemphasize recent events or information about a particular investment (or investment opportunity) for example, AI driven tech stocks, rather than looking at the big picture and historical data. This can lead to irrational decision-making such as chasing trends or selling prematurely.

Action bias is the cognitive tendency to prefer taking action over inaction. This bias persists even when doing nothing, i.e., consciously sticking to your plan is the more rational or beneficial choice. Hence the title for this post.

By the way, doing nothing doesn’t mean neglect. It means staying disciplined, aligned with a long-term plan, and avoiding reactive changes when your goals, time horizon, and fundamentals haven’t changed.

For starters, the plans we build for clients automatically factor in volatility. Even with a 10% portfolio decline, the overall likelihood of a client’s plan succeeding usually changes very little.

What warrants making a change?

There are times, however, when taking action is appropriate, such as going through major life changes (new child or grandchild, job loss, retirement, divorce) as well as portfolio drift, or strategic opportunities like rebalancing or tax-loss harvesting. The difference is intentional action vs. emotional action.

Portfolio drift is one of the trickiest changes to handle because it often flies under the radar. For instance, if your plan calls for a 60/40 allocation (stocks to bonds) and the stock market goes on a run or if your tech holdings are surging, you could be at 65/35 or even 70/30 before you know it. If you’re a Novi client, we’re constantly monitoring your portfolio. When it starts to “drift,” we’ll opportunistically trade, following the objective of selling high and buying low. There is little evidence that staying with that one winning position (momentum investing) is better than rebalancing.

But when it comes to short-term headline-driven volatility in the market, inaction is often the best course of action. Staying invested and properly diversified historically outperforms market timing. When the markets are dropping sharply, like they did last April when Trump tariffs were announced, a few worried clients called me wanting to go to all cash. Fortunately, I talked them out of it and the market went on a great run after that. They made up all the lost ground and more. But if I had let them go to all-cash, they would have missed out on a 20-plus percent rebound and possibly never recovered. Another example involves a client reaching out to me on the exact bottom day of a market correction. He was adamant about going to all cash because he thought the dip was just the beginning of something worse. Mind you, this was from a very smart professional who was also pretty young at the time. In other words, he had a lot more time to recover than a retiree or near-retiree would have. I finally talked him out of cashing in all his investment chips and protected him from his biases. Needless to say, he stayed the course, and his portfolio has been way, way up since then. But at the time, he was pretty angry with me for convincing him to stay in the market and was convinced he’d lose his nest egg. It may feel good at the time if you take action or require your advisor to take action. If you are not pausing or your advisor is not educating you, please reconsider your approach.

As the chart below shows, missing just the 15 or 25 best days in the market because you’ve temporarily gone to cash can have a devasting long-term impact on your wealth. We just never know when those 15 or 25 best days will occur, although they often come shortly after terrible days. Study after study shows the best way to win the investing game is to stay in the market and stay diversified. You never know which part of the market is going to recover, when, how fast and for how long.

Conclusion: Uncertain times like these are when your advisor can make a huge difference by keeping you grounded and focused on the long-term success of your plan. Don’t hesitate to reach out if you or someone close to you has concerns about your portfolio allocation or near-term turbulence in the markets, I’m happy to assist.

BRENDEN LEESE, CFP® is a Wealth Advisor at Novi Wealth Partners